1. PIT / CIT tax exemptions.

Pursuant to the Act on supporting new investments, the Polish Investment Zone has been operating throughout Poland since June 30, 2018. The public aid can be used by entrepreneurs from the entire territory of the country, not only from the areas covered by the zones. On January 1, 2022, an amendment to the act entered into force, which is largely related to the change in the regional aid map.

Type of support

Support under the Polish Investment Zone is granted in the form of CIT exemption or PIT exemption in connection with the implementation of a new investment. The tax relief is a regional investment aid. The percentage of public aid (i.e. aid intensity) depends on the size of the entrepreneur and the selected location.

What is the amount of support?

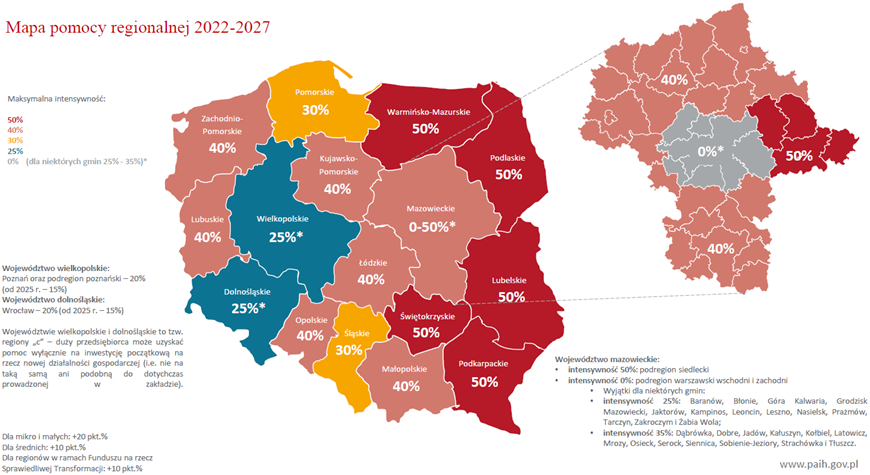

The amount of public aid in the form of CIT or PIT exemption is determined on the basis of the regional aid map for 2022-2027 (representing% of the costs eligible for regional aid):

Support for medium and small / micro enterprises is increased by 10 and 20 percentage points, respectively. For the Lubelskie Voivodeship, the maximum amount of support is 70% (for small and micro companies), 60% (for medium-sized companies) and 50% (for large companies).

For how long is the tax exemption granted?

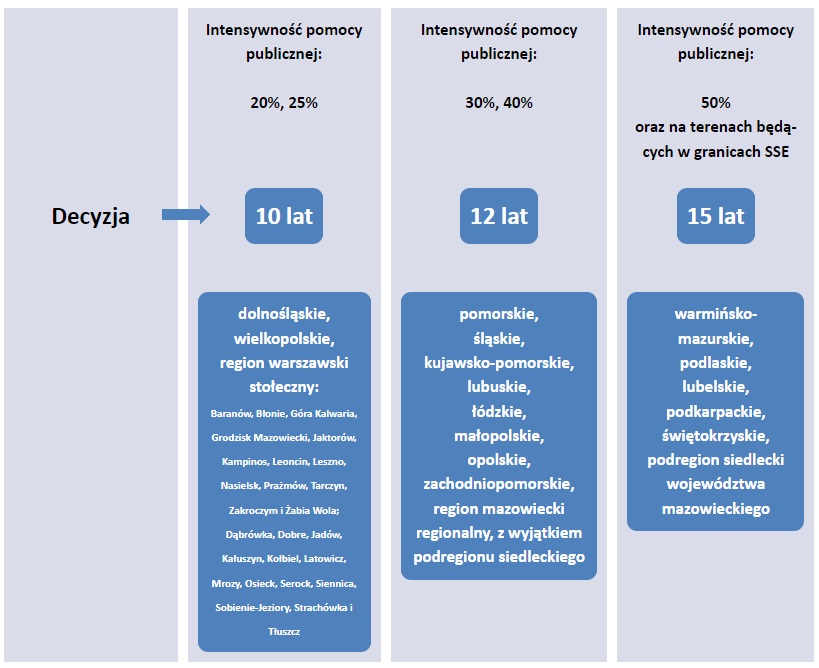

The period for which the decision on support is issued depends on the intensity of public aid for a given area. The time to use public aid is the same for all companies, regardless of the type of business and the size of the company. The decision on support is issued for a specified period of time, not shorter than 10 years and not longer than 15 years. The period of exemption is counted from the date of receipt of the decision on support and amounts to:

What are the criteria for receiving state aid?

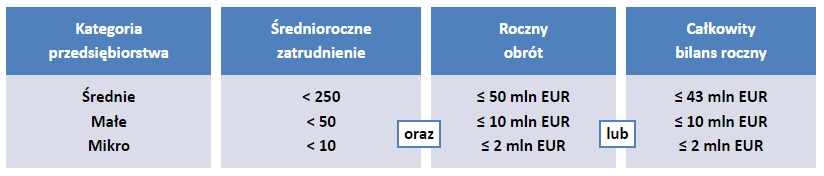

The decision on support is issued for the implementation of a new investment that meets certain quantitative and qualitative criteria. The quantitative criteria (minimum amount of eligible costs) depend on the unemployment rate in the poviat in which the investment will be implemented (the higher the unemployment rate, the lower the required amount of costs) and the size of the enterprise. Preferences were also granted to entrepreneurs conducting research and development activities and in the modern business services sector.

Detailed information on the Polish Investment Zone can be found at:

www.paih.gov.pl/strefa_inwestora/Polska_Strefa_Inwestycji

www.biznes.gov.pl/pl/polska-strefa-inwestycji

2. Real estate tax exemption.

In addition, the Lubartów Self-government has established real estate tax exemptions for a period of 2 years for new investments in the city.

Resolution NR XXIV/185/2020

Resolution NR LII/283/14